- Market Information

Is this the Brexit effect?

While hiring in Asset Management Sale across EMEA has fallen by 25% since 2014, hiring in the UK has falled 37%. Is this the Brexit effect?

- April 16, 2024

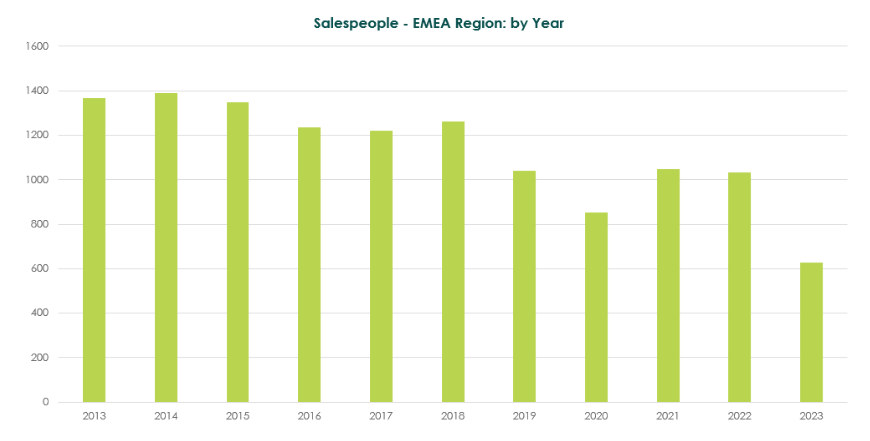

We’ve previously discussed the decade-long dip in hiring for sales roles across the EMEA Buy Side – down 25% since 2013. The reasons are well-known: industry consolidation, technological disruption, the rise of passive funds and ETFs, fee compression, increased regulatory and compliance costs, and Brexit, among others.

Last year’s 39% hiring slump was likely a response to dwindling RFPs and mandates as asset owners allocated to liquidity strategies amidst rising inflation and market instability from the summer of 2022.

Trends in hiring salespeople in asset management

Our latest data shows no signs of recovery yet. Hiring in Q1 2024 was down sharply from 2023, marking the 6th consecutive quarter of low demand since the summer of 2022. However, we anticipate a hiring surge soon, for six reasons:

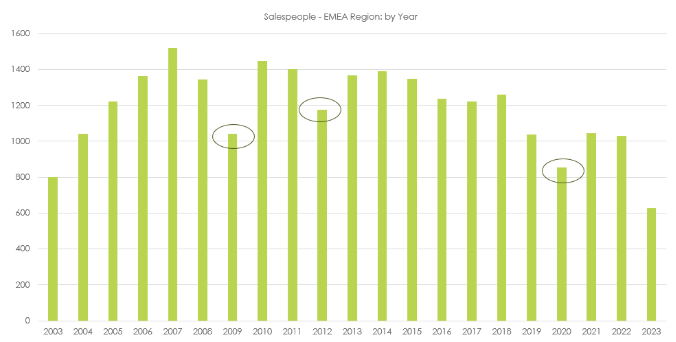

1. History Repeats: Past hiring slumps have always been followed by a bounce-back. We saw this in 2009, 2012, and 2020. Each time, hiring rebounded sharply the following year.

2003 to 2024 trends in asset management recruitment

2. The Big Switch: High inflation led many asset owners to temporarily shift allocations to liquidity products: Global Passive Equities, Money Markets, Short-dated Bonds, etc. However, most believe the strategic asset allocation (SAA) shift is inevitable. When it happens, sales teams will have a field day across a broader range of active strategies, boosting hiring demand.

3. Too Much De-Layering: After the initial COVID-19 shock, many firms resumed hiring at 2019 levels. But as market volatility and inflation rose, profits fell, and firms cut costs in early 2023. Many senior staff were let go as they offered the most bang for the buck, in terms of cost-savings. But when the market picks up, firms will likely need experienced leaders, boosting demand for senior sales roles.

4. No Meat on the Bone: In the quest for cost-savings, many firms have made do with less staff. Leavers have not been replaced. Teams are stretched thinly, and only just coping. When the market turns, they’ll likely need to hire more to cope with increased business activity.

5. Growth of Sales ‘Verticals’: As traditional DB markets shrink, asset managers are seeking new pools of assets by focusing on sales ‘verticals’ in areas like Alternatives, Insurance, and Financial Institutions Groups. This will require specialist skills, boosting hiring demand. By the way, Godliman has mapped all three verticals in anticipation of this upturn.

6. European Economic Recovery: Despite challenges like high inflation and geopolitical tensions, there are clear signs of economic recovery in Europe. A noticeable decline in headline inflation rates, with projections showing a decrease to around 2% by the European Central Bank’s target, could trigger the long-awaited SAA switch.

Most of our contacts remain convinced that the long-anticipated asset allocation switch is not an ‘if’ but a ‘when’. For the time being, while interest rates remain high, there is little incentive for Asset Owners to make any decision, as they are receiving a (relatively) risk-free 5.5% rate of return from money markets. But, once interest rates look set to fall, then the flow of mandates is likely to resume and this will likely be the catalyst to boost hiring numbers.

While hiring in Asset Management Sale across EMEA has fallen by 25% since 2014, hiring in the UK has falled 37%. Is this the Brexit effect?

Last year, hiring in buy side distribution across the EMEA region dropped by 43% compared to 2022.